Editor's Note

This editor’s note highlights the key facts and market implications behind “Building Materials Industry Landscape: Key Trend”, with emphasis on sourcing, product fit, fabrication, logistics, or buyer impact.

Infrastructure spending and fiscal policies are driving robust growth in the building materials sector. The building materials industry forms the literal foundation of our global infrastructure. From the cement in our bridges to the aggregates in our roads, these materials are essential for economic growth and development. Currently, the sector is experiencing a significant uplift, driven by supportive fiscal policies in major economies like the United States and Germany. Understanding these shifts is key to navigating the opportunities and challenges ahead. This article explores the key trends, market segments, and competitive dynamics that are shaping the future of building materials.

Key Market Trends for the Building Materials Industry

Two key government initiatives are fueling this boom. In the United States, the Infrastructure Investment and Jobs Act still has 60% of its highway funds waiting to be deployed. In Germany, a massive EUR 500 billion infrastructure fund was approved in 2025, with funds scheduled for deployment over the next 12 years. These long-term commitments provide a stable and predictable demand for building materials.

The Building Materials Industry Segment Analysis

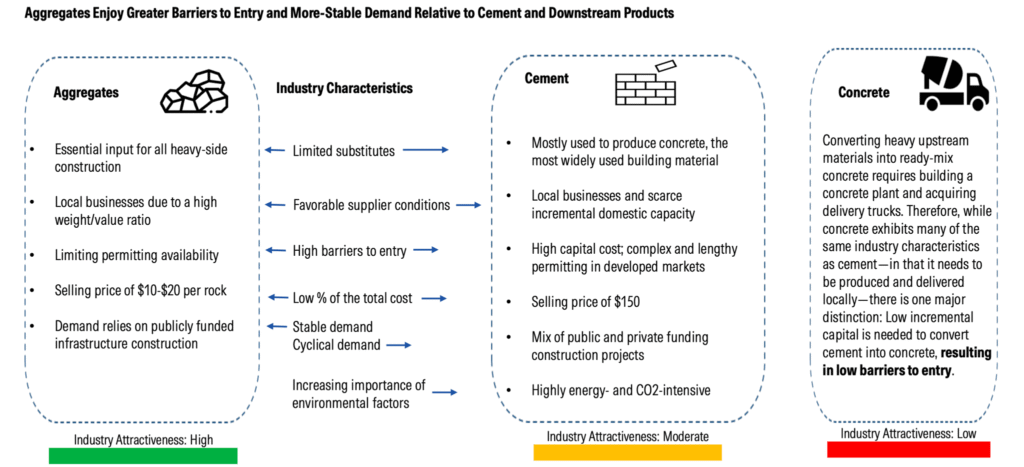

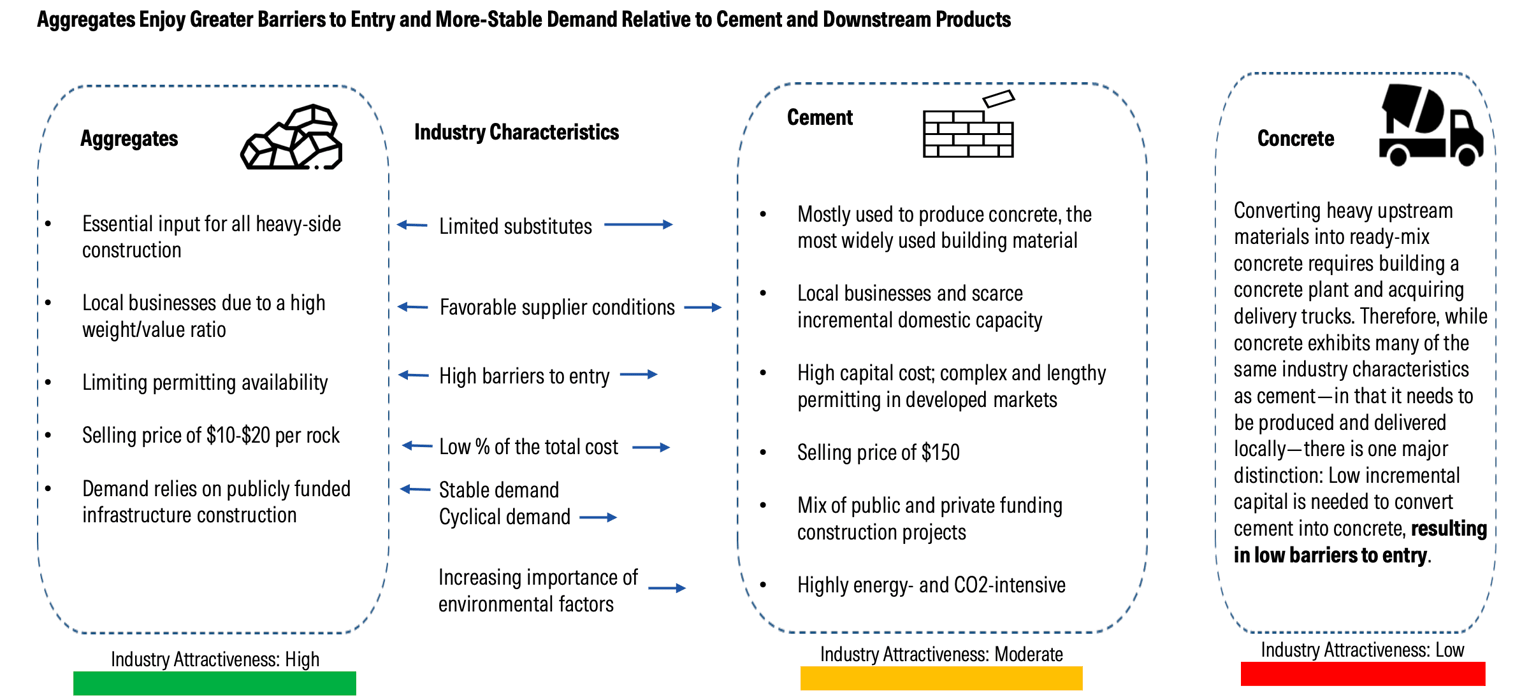

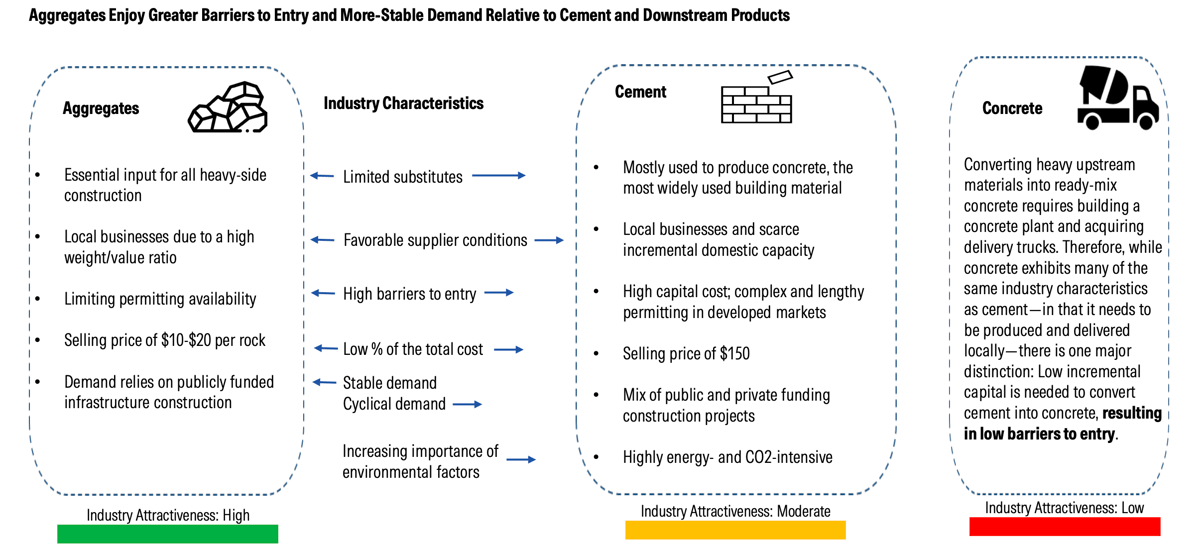

While often grouped together, the building materials industry consists of distinct segments, each with its own market dynamics. Aggregates—materials like sand, gravel, and crushed stone—are the unsung heroes of heavy-side construction. They are essential components of concrete and asphalt. As noted in the report, this segment benefits from significant barriers to entry and more stable demand compared to cement and other downstream products. Because aggregates are fundamental to nearly all construction, their demand remains consistently high.

Is Building Materials a Competitive Landscape?

Yes, the building materials market structure varies significantly by region and material type, creating a complex competitive environment.

At a global level, the building materials market is highly fragmented. This is largely due to the local nature of these markets; high transportation costs make it uneconomical to ship heavy materials over long distances. The push for decarbonization is one of the most transformative forces in the building materials industry today. With cement production alone accounting for roughly 6% of global carbon dioxide emissions, both regulators and customers are demanding greener solutions. The building materials industry is at a pivotal moment. Unprecedented government investment in infrastructure is securing a strong demand pipeline for years to come. Simultaneously, the urgent need for decarbonization is spurring innovation and reshaping the competitive landscape. A renewed focus on infrastructure, combined with a powerful push toward sustainability, is creating a dynamic environment for companies and investors.

Key Takeaways

Two major trends are defining the current landscape: a surge in infrastructure spending and the persistent pricing power of essential materials. An Infrastructure Spending Boom Governments are injecting massive capital into infrastructure projects, which is set to be a primary growth driver for years to come. Projections show that infrastructure construction spending will outpace both residential and non-residential building construction over the next five years. Durable Pricing Power This increased demand, backed by strong fiscal support, has allowed producers of core materials to maintain strong pricing power. US cement and aggregates, in particular, have shown remarkable price durability. This trend shows a steady upward trajectory. This pricing strength signals healthy profit margins and revenue stability for well-positioned companies in the sector.

Cement and Concrete are Global Industry Staples

Cement is the key ingredient used to produce concrete. After water, concrete is the most widely consumed product on the planet. Its versatility and strength make it indispensable for everything from skyscrapers to sidewalks. The global scale of cement consumption is staggering.

A Tale of Two Markets

However, certain regional markets are highly concentrated. In the United States, for example, the top 10 cement producers control nearly 90% of the region’s total capacity. This creates a market dominated by a few large players, with companies like Amrize holding a significant 18% capacity share. The Fragmented US Aggregates Industry In contrast to the consolidated US cement market, the US aggregates industry remains highly fragmented. The top five producers hold only about 35% of the market share. This fragmentation suggests a landscape with more intense local competition and potential opportunities for consolidation.

Technological Innovations and Sustainability

The Rise of Low-Carbon Alternatives The push for decarbonization is one of the most transformative forces in the building materials industry today. With cement production alone accounting for roughly 6% of global carbon dioxide emissions, both regulators and customers are demanding greener solutions.

Source: Read the original article | Published: January 07, 2026