Editor's Note

This editor’s note highlights the key facts and market implications behind “Size, Share, and Trends of the Wood-Based Panels”, with emphasis on sourcing, product fit, fabrication, logistics, or buyer impact.

Wood-based panels are engineered sheet materials manufactured by binding wood elements such as veneers, fibers, strands, or particles using adhesives under controlled heat and pressure to achieve consistent structural and surface properties. These panels are designed to optimize the use of wood resources by converting logs, residues, and recycled wood into standardized products with predictable strength, dimensional stability, and workability. They are widely used in furniture manufacturing, interior fit-out, cabinets, and shelving, where price sensitivity and standardized dimensions are essential. Advances in surface lamination and low-emission resins have improved their acceptance in residential interiors. Growing urbanization, affordable housing, and the expansion of furniture manufacturing capacity in Asia-Pacific and Eastern Europe continue to support demand.

Technological Advances in Panel Pressing, Surface Finishing, and Digital Printing

Technological advances in panel pressing, surface finishing, and digital printing have become a major trend shaping the global market. Continuous press systems and improved hot press control technologies enhance panel density uniformity, thickness accuracy, and production efficiency, allowing manufacturers to increase output while reducing defects and energy consumption. Advances in surface finishing, such as synchronized embossing, advanced laminates, and UV-cured coatings, enable panels to faithfully replicate natural wood, stone, and textured surfaces at lower cost. Meanwhile, digital printing technologies enable short production runs, rapid design changes, and high-resolution decorative customization for furniture and interior applications. For example, modular kitchen and storage systems widely use laminated MDF and particleboard cores for consistent surface quality and hardware mounting. Increasing urbanization, smaller living spaces, and online furniture sales are further accelerating demand for panel-based furniture.

Medium-Density Fiberboard (MDF) Segment

The Medium-Density Fiberboard (MDF) segment is characterized by its smooth surface finish, uniform density, and superior machinability, making it ideal for decorative and precision applications. It is widely used in furniture fronts, doors, moldings, wall panels, and interior decoration where paintability and design flexibility are essential. The expansion of modular furniture, interior renovation, and custom design solutions is driving MDF consumption. The segment is expected to grow at a CAGR of 3.7% during the study period.

Furniture Segment

The furniture segment held the largest share of 52.8% in 2025 due to the widespread use of particleboard and MDF in modular, ready-to-assemble, and mass-market furniture. Panels offer dimensional consistency, ease of machining, and cost control, which are essential for large-scale production. The growth of urban households, increasing demand for space-saving furniture, and the expansion of online furniture sales support panel consumption. Trends in interior customization, including laminated and digitally printed surfaces, are further increasing panel use. For heavy machinery, electronics, and export goods, panels offer better dimensional stability and efficient material use compared to solid wood. The growth of global trade, industrial manufacturing, and logistics supports demand.

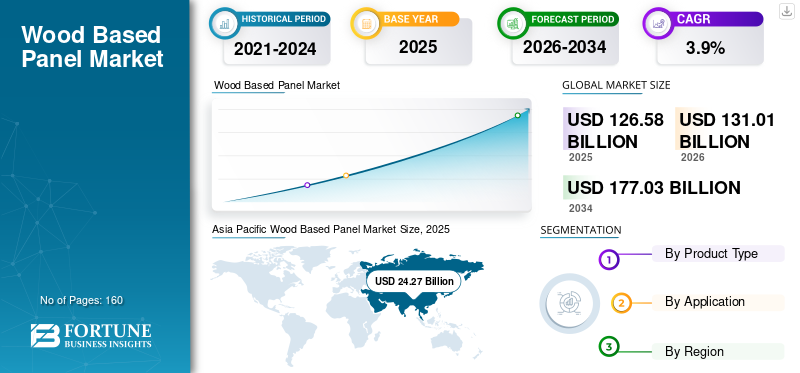

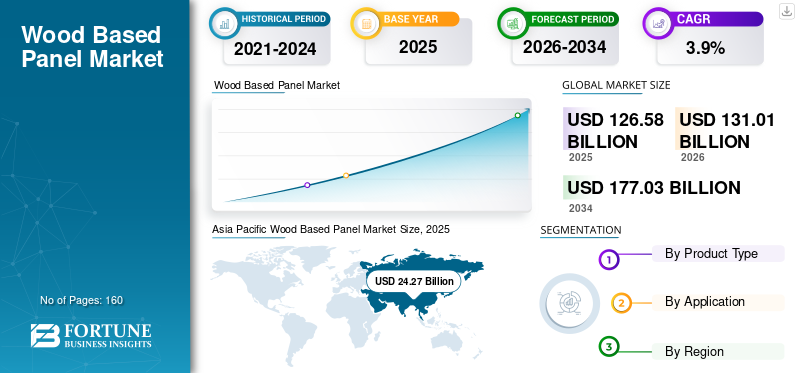

Asia-Pacific Region

Asia-Pacific held the dominant share in 2025, valued at $24.27 billion, and is expected to retain this dominant share in 2026 at $25.08 billion. Growth is driven by urbanization, housing construction, and furniture manufacturing capacity expansion. China dominates regional production and consumption, supported by large-scale panel manufacturing and export-oriented furniture industries. Rising middle-class incomes in India, Southeast Asia, and other emerging markets are fueling demand for affordable furniture and interior solutions. Particleboard and MDF are experiencing strong growth in modular furniture and cabinet markets, while OSB panel adoption is gradually increasing in the construction sector. In 2025, the Chinese market reached $24.76 billion due to its vast furniture manufacturing base, construction activities, and export-oriented production. Particleboard and MDF dominate due to their intensive use in ready-to-assemble furniture, cabinets, and interior fit-outs, while plywood remains important in construction and packaging.

Source: Read the original article | Published: March 23, 2026